- Embrace the Power of Life Insurance

- Determining Your Insurability

- Determining Your Life Insurance Needs

- The DIME Method

- Comment below or contact us to sign up for our FREE workshops.

Understanding the distinction between insurance and investment is vital for creating a solid financial strategy. Both tools serve different yet complementary purposes in managing risk and building wealth.

Insurance primarily acts as a safety net—designed to protect financially against unexpected events that can profoundly impact your life, such as illness, accidents, or death. For example, imagine a homeowner who pays roughly $500 annually to insure a house worth $500,000. If the home suffers catastrophic damage, like a fire, the insurance policy will provide the homeowner with the full amount necessary to rebuild or repair. Thus, a modest annual premium can safeguard against a potentially devastating financial loss.

In contrast, investment focuses on growing your capital over time, facilitating long-term financial goals, such as saving for retirement, funding children’s education, or achieving significant purchases. For instance, investing in a diverse portfolio comprising stocks, bonds, and real estate might generate substantial returns if managed well.

While insurance and investment might appear to be separate financial domains, they can serve similar functions when viewed through the right lens. In the early stages of life, individuals often prioritize obtaining adequate insurance to protect dependents. For example, a young parent could purchase a life insurance policy costing around $500 per year to ensure a benefit of $500,000 in the event of their untimely passing. This expense can be perceived as a necessary and crucial investment in family protection.

Conversely, as individuals age and accumulate wealth—perhaps achieving a net worth of $1,000,000 through diligent saving and investments—they might find themselves in a position where traditional life insurance is no longer vital; they have become “self-insured.” This transition illustrates how the roles of insurance and investment can evolve throughout different phases of life.

Whether your financial resources are directed toward insurance or investments, both paths can lead to the same goal: achieving financial independence.

Embrace the Power of Life Insurance

While life insurance may not be the most exciting topic, it is critical to your long-term financial strategy. The general public often avoids discussing it; many are unaware of its significance, leading to a lack of awareness that can jeopardize family financial stability. According to a 2020 study by the Insurance Information Institute, about 46% of American adults have no life insurance, placing their families at unintentional risk.

In everyday life, individuals readily purchase various forms of insurance—such as coverage for homes, vehicles, and even travel—but skepticism prevails regarding life insurance. However, life insurance is designed to protect families from financial hardship in the wake of a loved one’s death. It does not insure your life directly but secures your family’s ability to maintain financial stability without the burden of debts or lost income. Many people believe they do not need life insurance until they are older. However, acquiring life insurance at a younger age can significantly reduce premiums and provide a level of financial security that is often overlooked.

Many individuals opt for employer-sponsored group life insurance, assuming it will suffice. While this might seem convenient, coverage through an employer is often inadequate. For instance, according to the Bureau of Labor Statistics, only about 32% of employers typically provide coverage that sufficiently supports a family’s needs. Additionally, if the employment situation changes—due to job loss or career transition—this coverage may vanish, leaving individuals vulnerable.

Determining Your Insurability

Most companies require life insurance policyholders to undergo medical exams and provide health records before approval. Those with pre-existing health conditions may not only face higher rates but could also find their applications denied—a process similar to how auto insurance evaluates risk based on driving records.

Shockingly, many individuals may not even realize they are uninsurable. According to the American Heart Association, approximately 80 million Americans currently live with one or more forms of heart disease. Additionally, the National Cancer Institute asserts that 1 in 2 men and 1 in 3 women will receive a cancer diagnosis at some point in their lives. With statistics like these, the importance of securing life insurance early becomes evident, as waiting until health issues arise may render individuals uninsurable.

Those seeking immediate coverage have some options: policies can be issued without medical exams or with limited medical inquiries. However, these “guaranteed” policies typically have higher premiums and lower coverage limits. Purchasing life insurance while in good health can significantly enhance coverage quality and affordability, as healthier individuals often qualify for lower premium rates.

Determining Your Life Insurance Needs

Determining adequate life insurance coverage can be far more complex than equating it to your assets’ value. Unlike car or home insurance, where coverage amounts can be relatively straightforward, life insurance involves a multifaceted approach that considers current debts or assets and future responsibilities, such as income replacement, educational expenses for children, and any outstanding mortgages.

For example, suppose a primary earner in the family makes $100,000 annually. In that case, financial advisors frequently recommend having life insurance coverage amounting to 10-15 times that income, translating to a coverage range of $1,000,000 to $1,500,000. This principle ensures families maintain their lifestyle and cover significant expenses after a loss.

In addition, one should consider specific liabilities—such as mortgages, car loans, and credit card debts—as well as planned expenses like college tuition for children or even funeral services. Tools such as life insurance calculators on websites like Policygenius or Quotacy can provide personalized estimates of how much coverage you might need based on your financial situation and family structure.

Life insurance is not merely a financial product but a crucial element of sound financial planning. Approaching this decision with knowledge and foresight can significantly impact your family’s future stability and well-being. Investing the time to understand your options can lead you toward greater security and peace of mind.

The DIME Method

Many individuals secure policies with coverage amounts of $100,000, $200,000, or even $300,000 when it comes to life insurance. However, these figures often fall short of addressing their actual financial needs. The DIME method provides a constructive approach to determining life insurance coverage.

Calculating Your Protection Needs

Illustrative Example:

Client A:

While many people prioritize insurance for their homes and cars, it’s equally crucial to safeguard your family’s financial future.

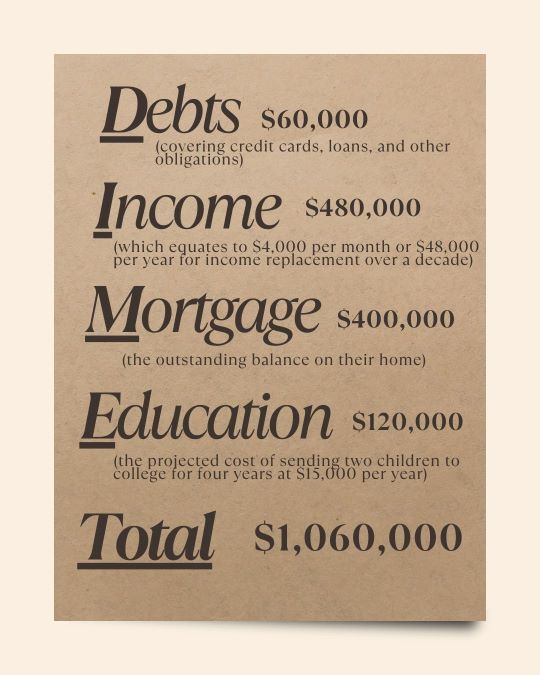

With a life insurance coverage of $1,060,000, Client A’s family would be well-supported if anything were to happen to them. The surviving spouse could pay off the $60,000 in debt, receive $4,000 monthly for 10 years for income replacement, settle the remaining $400,000 mortgage to keep their home, and ensure there’s $120,000 for the children’s college education.

The DIME method empowers you to assess your insurance needs effectively. Many individuals may realize they lack sufficient coverage to protect their loved ones. Research by the Life Insurance and Market Research Association (LIMRA) shows that only 44% of U.S. households have individual life insurance, and frequently, that protection is inadequate.

It’s common for people to say, “I have life insurance!” but it’s essential to ask: Is that coverage enough? Think about it: if your $400,000 home suffered a loss and you only had insurance for $50,000, your bank would require you to have the right coverage in place, so why not apply the same logic to life insurance?

Consider how your spouse and children would cope if they received only $100,000 after your passing. After handling immediate expenses, they could be left financially vulnerable and face significant challenges.

The DIME Method is a valuable resource to help clarify your life insurance needs. Individual circumstances vary, so consulting with an insurance agent or professional can ensure you tailor your coverage to fit your unique situation effectively.

http://www.limra.com/uploadedFiles/limracom/Posts/PR/LIAM/PDF/Facts-Life-2013.pdf

Leave a comment