Benjamin Franklin’s famous adage rings true: death and taxes are the only certainties in life.

When you begin earning income, you find yourself subject to taxation. You receive a paycheck, and a portion of your hard-earned money is withheld for income tax, contributing to government funding and programs.

When you make a purchase, that money doesn’t escape unscathed, as sales tax is imposed on the goods and services you acquire. Even when you attempt to save for the future, you find that interest earned in savings accounts can also be taxed, reducing the rewards of your diligence and foresight.

And then, after a lifetime of navigating these financial obligations, when you pass away, the government still lays claim to a part of your estate through estate taxes or inheritance taxes, ensuring that even in death, they continue to take their share.

From property taxes levied on the real estate you own to myriad other forms of taxation, tax collectors are omnipresent, always ready to claim their rightful portion of your finances. Every phase of life feels like a relentless cycle, reminding us of the inescapable grip of taxation.

Taxation is an inevitable reality of our lives, touching nearly every financial aspect. From sales taxes on everyday purchases to income taxes that take a portion of our hard-earned wages, these contributions shape our economy. Property taxes fund essential local services like schools and infrastructure, while estate taxes aim to ensure a fair transfer of wealth between generations. Tax collectors play a crucial role in this system, ensuring everyone fulfills their obligations. Understanding the importance of these taxes helps us appreciate their role in supporting our communities and public resources.

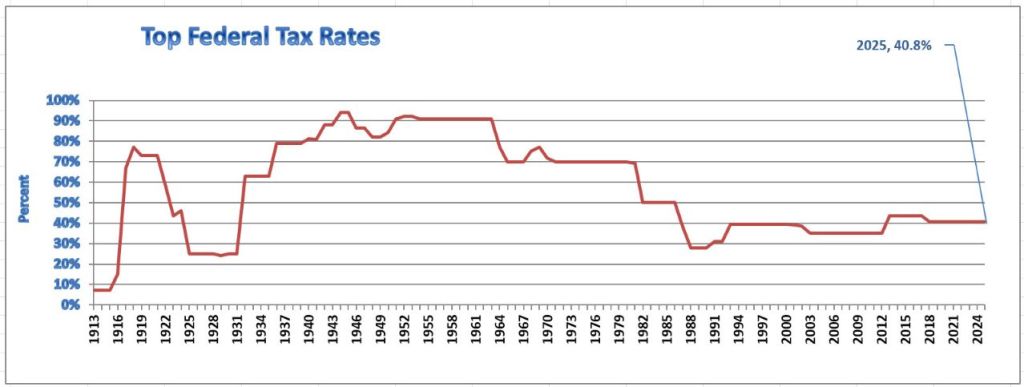

However, there is a silver lining: the highest current U.S. federal income tax rate is strikingly low compared to historical levels. It soared over 90% during President Kennedy’s tenure and hovered around 70% at the start of the Reagan era. Today’s top federal tax bracket is more manageable, but don’t be fooled—when you factor in state income taxes, your total tax burden can be significantly higher. For the latest tax rates, visit http://www.irs.gov.

- As adjusted by the Consumer Price Index Inflation Calculator from the U.S. Department of Labor, Bureau of Labor Statistics at http://www.bls.gov/data/inflation_calculator.htm.

- For simplicity, unless otherwise noted, the historical federal income tax rates in this article refer to the highest tax rate.

- http://data.bls.gov/cgi-bin/cpicalc.pl

- http://www.irs.gov/pub/irs-soi/05inrate.pdf, p. 8

Canadians encounter a range of tax brackets and rates, along with distinct taxes such as the Goods and Services Tax (GST) and the Harmonized Sales Tax (HST). Regardless of these variations, the bottom line is clear: taxes diminish the money you take home. To learn about the current Canadian tax rates, visit http://www.cra-arc.gc.ca/tx/ndvdls/ fq/txrts-eng.html.

A Taxing Issue

Taxes significantly diminish your income, making it essential for any saving and investment strategy to account for their impact precisely. You must assess your current tax rate, anticipate what it might be in the future, and determine whether taxes are likely to rise or fall. Here are the pressing challenges we face:

- The Shrinking Tax Base

Since the inception of Social Security in 1945, the ratio of workers to retirees has plummeted from over 40 to about 3 today—and this decline is ongoing due to the aging demographics in the U.S. and Canada. Consequently, governments will find it increasingly difficult to maintain existing systems such as Social Security, the Canadian Pension Plan, and the benefits that seniors currently rely on. - Mounting Debts

As of January 2023, the U.S. national debt has surged to an alarming $31 trillion, imposing a staggering burden of approximately $93,000 on every citizen. This represents a dramatic rise from around $18 trillion just eight years ago. We must take decisive action now to confront this escalating financial crisis head-on.

Canada’s national debt is staggering C$692.4 billion, imposing an average burden of C$19,590 on each citizen.

It’s clear who will ultimately shoulder this debt: our future generations. The government relies heavily on public debt, borrowing from individuals, businesses, and foreign governments that purchase Treasury bills, notes, and bonds.

Foreign investors play a significant role in the U.S. national debt, with China and Japan leading the way, each holding over $1 trillion in American securities. This reality underscores the urgent need for fiscal responsibility and decisive action to manage our financial future.

As the ratio of workers to retirees continues to shrink, the costs of providing retirement benefits, Medicare, defense, and infrastructure are rising significantly. The government must make a critical decision: cut the budget or raise taxes. Many people are convinced that taxes will have to increase in the future. What is your stance on this issue?

Capital Gains Tax

Most items you own for personal use or as investments are considered capital assets. These include properties like your home and financial instruments such as stocks and bonds. When you sell these capital assets, the profit or loss you realize is determined by the difference between the sale price and your basis—typically the amount you initially invested.

If you hold an asset for less than one year before selling it, any gains incurred are classified as short-term capital gains and are generally taxed at your regular income tax rates. Understanding these distinctions is crucial for effective financial planning and tax management.

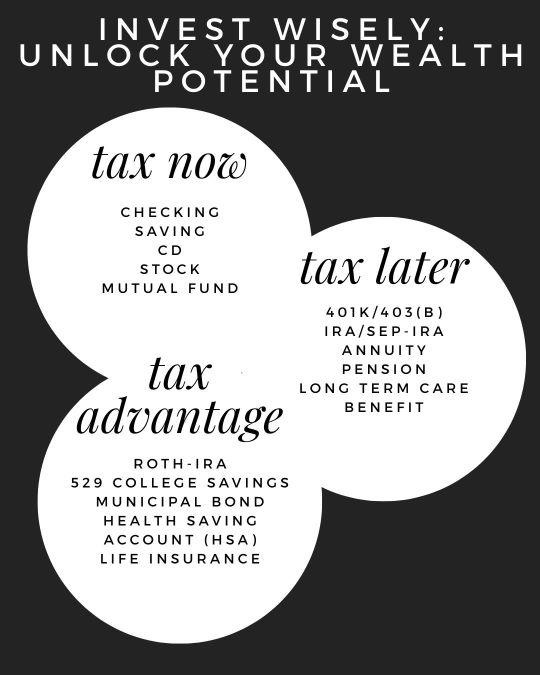

Tax Now – Tax Later – Tax-Advantaged

It’s time to take control of your finances. Let’s examine the tax treatment of different types of investment accounts to understand exactly where your money goes.

Tax Now

Tax regulations dictate that any earnings generated from various financial accounts are subject to taxation in the respective tax year. This includes earnings from savings accounts, Certificates of Deposit (CDs), dividends received from stocks, returns from mutual funds, and money market funds, all of which must be reported for tax purposes. In Canada, this taxation applies to Guaranteed Investment Certificates (GICs), Term Deposits, and any other investments or savings held in non-registered plans.

Tax Later

Tax later accounts, often referred to as tax-deferred accounts, allow individuals to deposit money without paying income tax upfront. This means the funds you contribute are considered pre-tax income, which has not yet been subjected to income tax. However, it is essential to understand that while you defer tax payments on these contributions, you will eventually owe taxes when you begin to withdraw the funds.

In the United States, typical examples of these tax-deferred accounts include Individual Retirement Accounts (IRAs), 401(k) plans, and 403(b) plans. These accounts are structured to promote retirement savings by deferring tax obligations until retirement age. In Canada, similar savings vehicles exist, including Registered Retirement Savings Plans (RRSPs), Registered Educational Savings Plans (RESPs), and Registered Disability Savings Plans (RDSPs). These accounts function under similar principles, allowing you to contribute pre-tax income while deferring taxes until funds are withdrawn.

In the U.S., the rules for withdrawing money from these accounts are specific. Once you reach the age of 59½, you can start taking distributions from your accounts without penalty; however, the amounts withdrawn will be taxed as ordinary income. If you withdraw funds before reaching 59½, you typically face a 10% early withdrawal penalty on top of the income tax owed. However, there are certain exceptions to this rule for specific circumstances such as disability or purchasing a first home. Furthermore, the IRS mandates that you withdraw a minimum amount from these accounts by the time you reach 70½ years of age, a requirement known as the Required Minimum Distribution (RMD).

It’s important to note that not all tax-deferred accounts offer tax deductions upfront. For instance, non-qualified annuities and non-deductible IRAs are accounts where the money deposited is considered after-tax income, meaning you’ve already paid taxes on those contributions. When you later withdraw funds from these accounts, you will only owe taxes on the earnings accrued, not on the initial contributions, as they have already been taxed.

Canadian RRSPs operate under slightly different rules but share a similar fundamental structure to their U.S. counterparts, allowing individuals to contribute pre-tax dollars. While individuals enjoy tax-deferred growth while the money remains within the RRSP, taxes will eventually be owed upon withdrawal, particularly when the funds are taken out during retirement. At that point, they are taxed as ordinary income.

For those interested in learning more about the specific rules, contributions, and implications of RRSPs, further information can be found at: http://www.cra-arc.gc.ca/tx/ndvdls/tpcs/rrsp-reer/rrsps-eng.html.

Tax-Advantaged

Tax-advantaged accounts are investment vehicles designed to minimize or eliminate tax burdens when you withdraw funds. This means that, generally, you won’t incur taxes on the money you withdraw from these accounts, allowing for more significant growth over time. The funds used in these accounts are typically considered after-tax money, meaning you have already paid taxes on them before making contributions.

Some popular tax-advantaged investment options include Roth IRAs, 529 College Savings Plans, Tax-Free Savings Accounts (TFSAs), and various life insurance products. These vehicles provide the benefit of tax-exempt distributions, allowing account holders to access their funds without additional tax liabilities during withdrawal.

In Canada, the Tax-Free Savings Account (TFSA) is particularly notable for its tax-exempt nature. Contributions to a TFSA are made with already taxed money, but any withdrawals, including investment gains, are entirely tax-free. This feature makes TFSAs an attractive option for individuals looking to grow their savings without worrying about tax implications.

Additionally, registered education savings plans (RESPs) and registered disability savings plans (RDSPs) in Canada offer varied tax advantages. These accounts often have characteristics classified as “Tax Later,” where taxes may apply at a different time, and “Tax Exempt,” where certain earnings can grow tax-free.

For a deeper understanding of the specific features, advantages, and rules surrounding these financial instruments, you can explore the details provided in the following sources: http://www.cra-arc.gc.ca/tx/ndvdls/tpcs/rdsp-reei/menu-eng.html and http://www.cra-arc.gc.ca/tx/ndvdls/tpcs/resp-reee/menu-eng.html.

Before Or After?

Deciding when to pay taxes on your investments is a significant financial decision that many individuals face. Specifically, Should you defer paying taxes until later in life or pay them now? This dilemma can be framed as whether to pay taxes on the “seed” (the initial investment) or on the “harvest” (the returns on that investment).

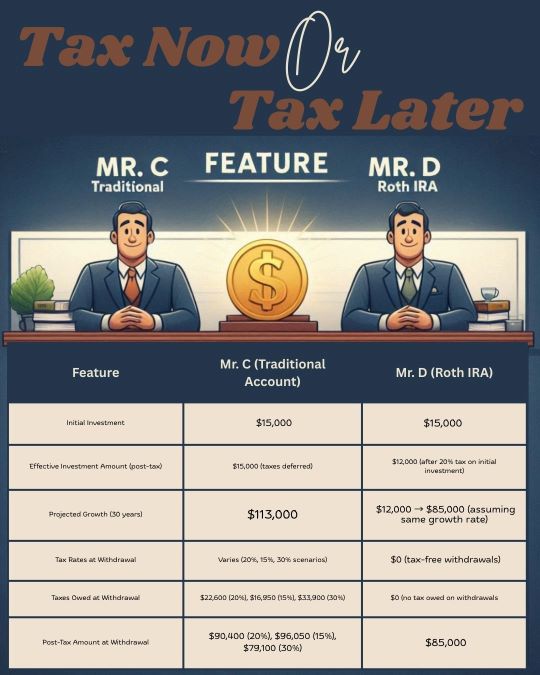

To illustrate various investment strategies in retirement planning, let’s consider two hypothetical individuals: Mr. C and Mr. D. Both have an initial capital of $15,000 that they are ready to invest in a retirement portfolio, which is projected to yield a 7% annual rate of return over the next 30 years. To help estimate how this investment will perform, we can use the Rule of 72, a simple formula that allows investors to calculate the years required for an investment to double. By dividing 72 by the annual rate of return (in this case, 7%), we find that their investments are expected to double every 10.3 years approximately.

Mr. C decides to invest his funds in a traditional retirement account. This type of account allows him to defer taxes until he begins withdrawing funds during retirement, potentially benefiting from a lower tax rate. Conversely, Mr. D opts for a Roth IRA, where he invests his money with taxes already deducted. While Mr. D pays taxes upfront on his initial investment, this strategy allows his investment to grow completely tax-free, meaning he won’t owe any taxes on withdrawals during retirement.

For the sake of simplicity, we assume that both individuals face a uniform tax rate of 20% when they eventually withdraw their funds. However, it’s important to note that tax rates can vary widely based on individual circumstances and changes in tax law.

After 30 years of compounding growth, Mr. C’s initial investment of $15,000 is projected to grow significantly, but taxes will need to be considered upon withdrawal. Let’s analyze three different scenarios for Mr. C’s tax situation at retirement:

Scenario with Constant Tax Rate: If Mr. C’s tax rate remains at 20% when he turns 65, his investment would grow to approximately $113,000. When he withdraws this amount, he would owe $22,600 in taxes (20% of $113,000), leaving him with a post-tax total of about $90,400. This scenario demonstrates the potential benefits of tax deferral but highlights the importance of understanding future tax implications.

Scenario with Lower Tax Rate: If Mr. C finds himself in a more favorable tax bracket of 15% at retirement, he would owe $16,950 in taxes (15% of $113,000). This would result in a net amount of $96,050 after taxes, illustrating a clear advantage of his tax-deferral strategy, as he retains a higher investment.

Scenario with Higher Tax Rate: If Mr. C’s tax rate increases to 30% by the time he withdraws his funds, his tax liability will rise significantly. He will then owe $33,900 in taxes (30% of $113,000), leaving him with only $79,100 after taxes. This scenario underscores a potential downside of Mr. C’s strategy—should tax rates rise significantly, tax deferral benefits may diminish, leading to a less favorable outcome than Mr. D.

On the other hand, Mr. D, by choosing to invest in a Roth IRA, pays taxes upfront. After accounting for the 20% tax rate, his initial investment of $15,000 would effectively amount to $12,000 available for investment. This approach allows his money to grow tax-free over the same 30-year period, free from future tax liabilities when he begins to withdraw funds.

As retirement approaches, this decision-making process illustrates the complexities individuals face as they navigate potential risks and uncertainties associated with future tax rates. While some investors resonate with Mr. C’s strategy, believing they will be in a lower tax bracket during retirement due to decreased income, others, like Mr. D, prefer the certainty of tax-free withdrawals. These considerations reflect broader concerns about potential tax increases or shifting economic policies that impact retirement income and overall financial security. Knowing these factors can help future retirees make more informed decisions about their investment strategies.

Ultimately, it is crucial to recognize that financial strategies regarding tax payments are not one-size-fits-all. They require a nuanced understanding of individual circumstances, financial goals, and potential changes in tax policy. Tailored planning is essential to identifying the best course of action for one’s personal financial landscape.

Leave a comment