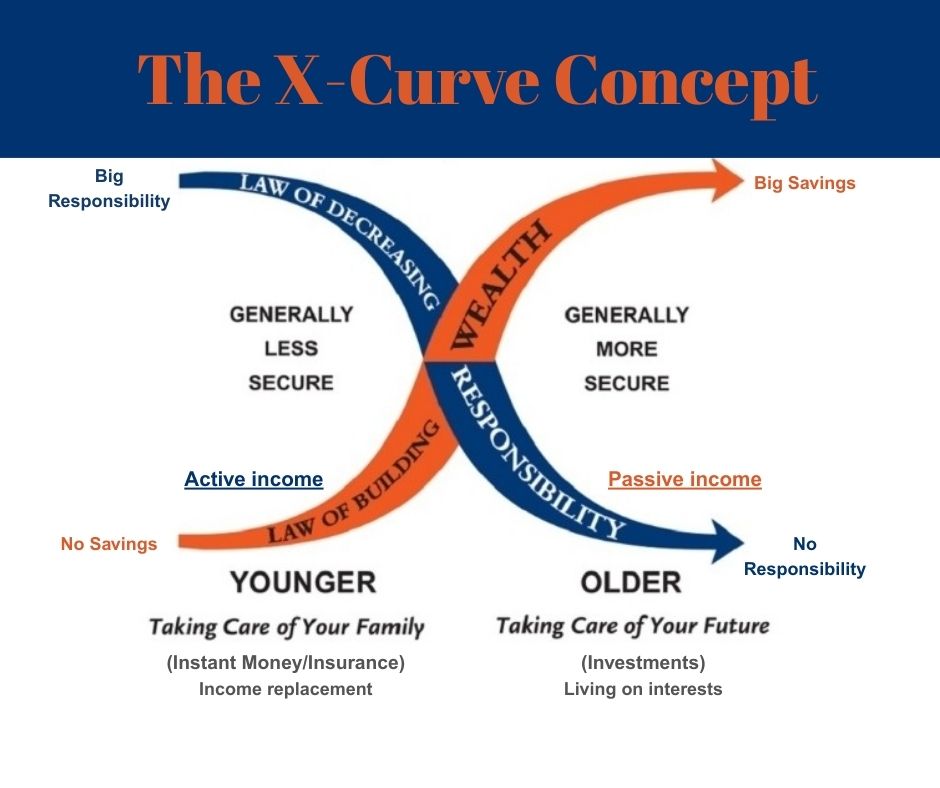

Embrace the power of the X-Curve Concept as it unveils the beautiful patterns of our journey, inspiring growth and transformation along the way.

- Creating Wealth the Right Way

- The Wealth Curve

- The Responsibility Curve

- More Wealth, Less Responsibility

- Conclusion

- Comment below or contact us to sign up for our FREE workshops.

Creating Wealth the Right Way

The X-Curve concept is an insightful framework designed to help individuals visualize and understand the complex interplay between their financial responsibilities and the accumulation process over their lives. This model posits that as a person’s financial obligations generally decrease over time, their wealth increases correspondingly. The resulting X-Curve consists of two distinct curves—one representing financial responsibilities and the other representing wealth—that move in opposite directions across different stages of life.

The Wealth Curve

In the initial stages of life, particularly during young adulthood, individuals often grapple with limited financial resources. Many find themselves taking on part-time jobs, burdened by student loans, or entering the workforce with modest starting salaries. This challenging financial landscape can leave little room for significant savings or investment.

However, as young adults begin to navigate and manage their finances more effectively, they typically embark on a journey aimed at wealth accumulation. This often involves opening savings accounts, contributing to retirement plans, and exploring investment options such as mutual funds or stocks. During this formative phase, the wealth curve starts to ascend, reflecting the gradual increase in income and accumulation of assets.

As individuals enter their prime earning years—usually in their 30s and 40s—they have a unique opportunity to build substantial wealth and secure their financial future. Career advancement, salary increases, and the potential for significant bonuses or additional income streams characterize this period. The upward trajectory of the wealth curve continues as individuals capitalize on these opportunities, with savings and investment portfolios growing. This curve illustrates how the sound financial decisions and disciplined saving practices established in earlier years lay critical groundwork for achieving long-term financial stability as one approaches retirement.

The Responsibility Curve

In stark contrast, the early years of adulthood often bring about a surge in financial responsibilities, particularly for those who choose to start families. This phase is marked by many obligations that can place immense financial stress. Key responsibilities often include raising children, managing a mortgage, saving for higher education, and effectively managing debt.

Raising children involves various financial responsibilities, including childcare, healthcare, and educational expenses. While these costs can be significant, planning and budgeting effectively can help manage them. Families can navigate these challenges by seeking resources and support and creating a secure and nurturing environment for their children.

A mortgage is often essential when buying a home, making it a significant long-term investment. Grasping this commitment will enable you to effectively manage your monthly budget and plan for a secure financial future.

Recognizing the rising costs of higher education, many parents proactively set aside funds to invest in their children’s future college or university education. This thoughtful planning can help ensure their children have the financial support they need to pursue their academic goals.

Young adults have a valuable opportunity to develop effective strategies for managing various types of debt, including student loans, credit card debt, and other financial obligations. They can navigate these financial challenges through careful planning and informed decision-making and work towards a prosperous and secure financial future.

During this stage of life, the weight of these financial responsibilities can create significant pressure. As a result, the need for adequate insurance protection becomes paramount. Life insurance, in particular, is critical for families, ensuring that dependents are financially secure in the event of an unexpected tragedy. However, as children mature and financial obligations evolve, such as decreasing debts or fully paying off the mortgage, individuals may find their overall responsibility diminishes over time. The need for insurance coverage may also decrease as one’s financial landscape stabilizes.

More Wealth, Less Responsibility

To better understand this principle, consider a scenario in which you have two children. If the unthinkable happens and you pass away unexpectedly, your spouse would likely face considerable challenges managing the family’s finances without adequate support. In this situation, assessing your family’s standard of living, existing debts, and financial aspirations may lead you to conclude that a life insurance policy providing $500,000 in coverage is essential to ensure your spouse can sustain the household and meet your children’s needs.

Over the years, you cultivate strong saving habits and amass $100,000 in savings. In this case, your total insurance need may decline to $400,000, as your spouse would have access to both your savings and the insurance payout in case of your untimely death, totaling $500,000 in financial support. If your savings grow to $300,000, your insurance requirement could be further reduced to $200,000. Ultimately, when you achieve $500,000 in savings or investments, the need for life insurance protection may diminish entirely, as your savings would provide a robust safety net.

Let’s also explore the implications of homeownership under this concept. When an individual purchases a home, their friends may celebrate this milestone. Still, it’s essential to recognize that, in reality, the bank holds ownership of the house until the mortgage is fully paid off. This presents a significant financial responsibility. For example, suppose you take out a mortgage of $300,000 over a 30-year term. In that case, a substantial portion of the early payments will be allocated to interest rather than directly reducing the principal amount owed.

In “The Power of Zero” by David McKnight, one prominent example he discusses revolves around tax-efficient retirement planning. McKnight emphasizes the importance of building wealth to minimize tax liabilities in retirement. One example he provides is the use of Roth IRAs, which allow individuals to contribute after-tax dollars and withdraw funds tax-free during retirement. By strategically using these tax-advantaged accounts, individuals can maximize their income while reducing the impact of taxes on their retirement savings. This aligns with the X-Curve concept, as it highlights the importance of managing financial responsibilities while accumulating wealth in a tax-efficient manner.

McKnight also illustrates scenarios where individuals can accumulate significant wealth by utilizing the right financial vehicles, effectively creating a balanced approach to wealth accumulation and responsibility management over their lifetime. This reinforces the idea that individuals can navigate their financial journey toward a more secure future with foresight and planning.

Recognizing the importance of the X-Curve enables individuals to make informed financial decisions, such as opting to pay more than the minimum on their monthly mortgage payments. Taking this proactive approach can significantly accelerate contributions to the mortgage principal, allowing homeowners to reduce their mortgage balance more quickly. This strategy can lead to achieving homeownership sooner than anticipated, inspiring individuals to take charge of their financial planning and make proactive decisions.

Conclusion

In conclusion, the X-Curve provides a clear and actionable strategy for establishing a solid financial foundation. Motivating individuals to save responsibly, invest wisely, and accumulate assets effectively encourages the gradual decrease of financial responsibilities over time while simultaneously building wealth. Understanding and applying the X-Curve concept lays the groundwork for enduring financial security throughout one’s lifespan and empowers individuals to take control of their financial future.

Leave a comment